Currently in Scotland LBTT applies to transactions involving land and buildings transactions, but on the 25th November 2015, the UK Government’s Autumn Statement proposed the introduction of a supplementary SDLT charge of 3% on the purchase of additional residential properties in England, Wales and Northern Ireland, to take effect from 1st April 2016.

John Swinney then announced on 16th December that Scotland would follow suit. The Scottish Government Draft Budget for 2016/2017 proposed the introduction of a supplementary LBTT charge of 3% on the purchase of additional residential properties in Scotland, also with effect from 1st April 2016. It is important that we make it clear that this is a transactional tax and will not affect landlords’ current properties.

It does, however, mean that any homeowner in Scotland wishing to buy a second home or buy-to-let property will face an additional tax charge of 3% payable on top of the current LBTT rate. The 3% supplement will be levied on all relevant transactions above £40,000, which is below the current threshold for LBTT. Initially, that 3 per cent doesn’t sound like much, but a buy-to-let investment of £145,000, currently free of LBTT, would now cost an extra £4350. The tax on a property costing £250,001 would rise from £2100 to £9600, while a £325,000 buy-to-let currently attracting LBTT of £5850 would from April have an added levy of £9750, making a total of £15,600.

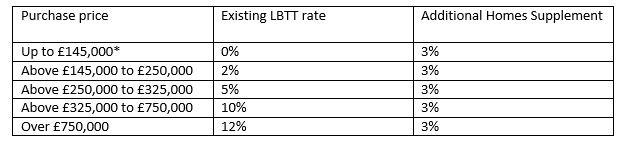

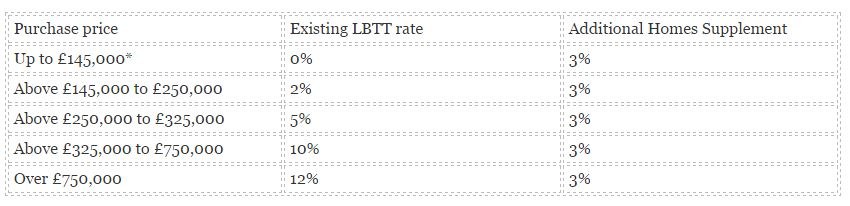

The hike is, in fact, worse than it first seemed because although LBTT doesn’t apply on properties up to £40,000, once you go above that level the initial 3% of LBTT will be applied to the whole purchase, not just the proportion exceeding £40,000. The proposed rates are outlined below (source www.gov.scot) :

| Purchase price | Existing LBTT rate | Additional Homes Supplement |

| Up to £145,000* | 0% | 3% |

| Above £145,000 to £250,000 | 2% | 3% |

| Above £250,000 to £325,000 | 5% | 3% |

| Above £325,000 to £750,000 | 10% | 3% |

| Over £750,000 | 12% | 3% |

*Supplement only payable on transactions on or above £40,000.

A calculator for the proposed LBTT supplement on the purchase of additional residential properties can be found on the Scottish Government’s website here:

http://www.gov.scot/Topics/Government/Finance/scottishapproach/devolvedtaxes/LBTT

As we await further details, here are a few things to remember:

- This is a transactional tax and will not affect landlords’ current properties.

- This comes on top of landlords soon losing the ability to offset all their mortgage interest against tax on rental income.

- It has been predicted that, as an unintended consequence, these changes could lead to an increase in rental rates as smaller investors try to recoup their increased costs directly from their tenants.

- The 3% supplement will not apply to individuals who own one main residential property, no matter what the intended use of the property may be, e.g. buy-to-let.

Given these looming changes, our predictions are that there will be a surge in property purchases this side of April 2016, due to everyone acknowledging the fact that purchasing will be notably more expensive once additional 3% is applied. We predict there will inevitably then be a surge in demand for properties, making the early months of 2016 an ideal time to sell.

To speak to a member of our team at McEwan Fraser Legal about valuation on your property please call 0345 210 2121.

{kind=link}

{kind=link}

{kind=link}